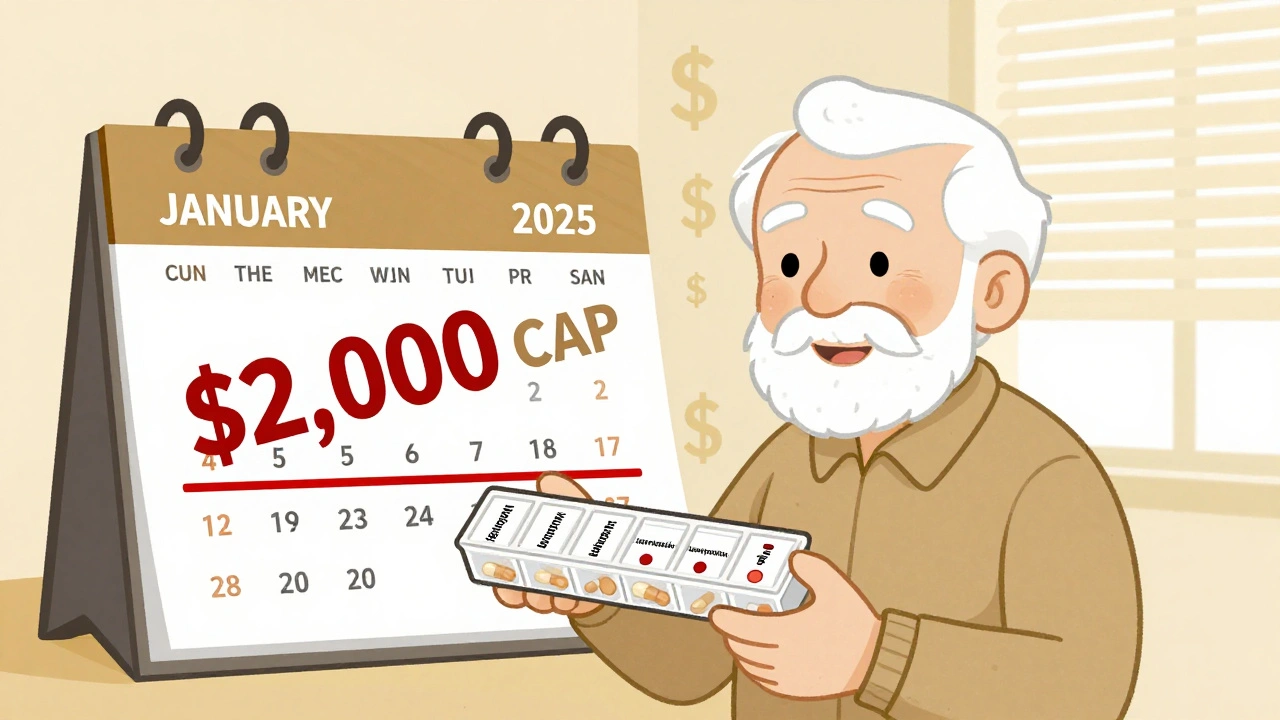

By 2025, Medicare Part D is simpler for people taking generic drugs than it’s ever been. If you’re on a fixed income and rely on medications like lisinopril, metformin, or atorvastatin, the system now works in your favor. The big change? Out-of-pocket costs for generics are capped at $2,000 a year - no more surprise bills in the middle of the year. That’s not a rumor. It’s federal law, effective January 1, 2025.

How Medicare Part D Formularies Are Built

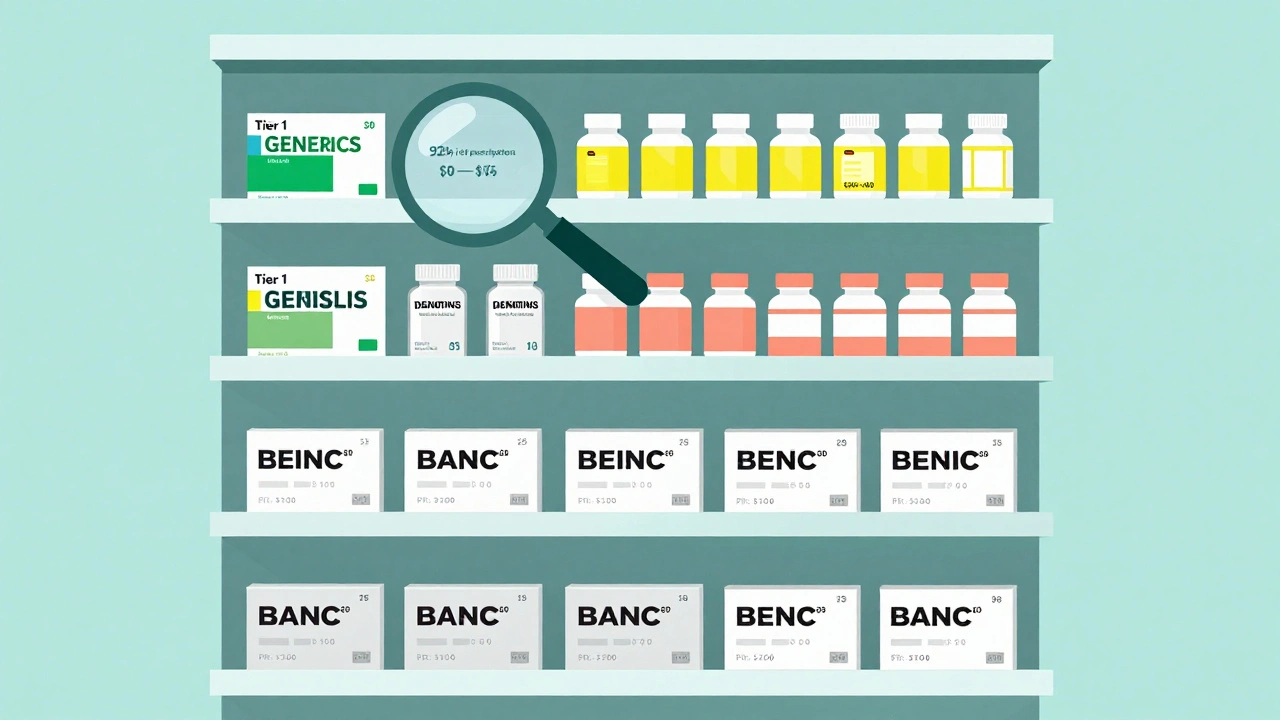

Every Medicare Part D plan has a list of covered drugs called a formulary. It’s not random. The government requires each plan to cover at least two different generic versions of every common medication type - like blood pressure pills or diabetes meds. This ensures you’re not stuck with just one brand of generic, even if your pharmacy runs out. Formularies are split into five tiers. Generics almost always land in Tier 1 or Tier 2. Tier 1 is for the cheapest, most commonly used generics. Think of it as the plan’s preferred list. These often cost $0 to $15 for a 30-day supply. Tier 2 includes generics that are slightly more expensive or less commonly prescribed. These might cost $20 to $40, or you might pay 25-35% of the drug’s price. The higher tiers - 3, 4, and 5 - are for brand-name drugs and specialty medications. That’s where the big costs show up. But if you’re only taking generics, you’re mostly staying in Tiers 1 and 2. And that’s where the savings happen.What You Pay for Generics in 2025

Here’s how your money flows in 2025:- Deductible: You pay the first $615 of drug costs. Some plans have $0 deductibles - 52% of them do. Check yours.

- Initial Coverage: After the deductible, you pay 25% of the cost for each generic drug. The plan pays 75%. This continues until your total out-of-pocket spending hits $2,000.

- Catastrophic Coverage: Once you hit $2,000, you pay nothing for the rest of the year. Not $1. Not a copay. Zero. Medicare covers nearly all the cost.

Why Generics Are So Much Cheaper

You might wonder why generics cost so little compared to brand names. It’s simple: generics are chemically identical to the original drug but don’t carry the cost of research, marketing, or patent protection. The FDA requires them to work the same way. So why pay $150 for a brand-name statin when a generic version costs $10? In 2023, 92% of all Part D prescriptions were for generics. But those generics made up only 18% of total drug spending. That’s because they’re cheap. A single brand-name drug can cost $500 a month. A generic version of the same drug? Often under $20. Plans encourage this by putting generics in the lowest tiers. They want you to pick them because it saves money for everyone - you, the plan, and Medicare.

What You Need to Watch Out For

Even with all the improvements, there are still traps. First, plans can change their formularies every year. A generic you’ve been taking for years might get moved from Tier 1 to Tier 2 - or even get removed entirely. That’s why you must read your Annual Notice of Change (ANOC) every fall. It’s mailed to you. It’s also online. Don’t ignore it. Second, not all generics are treated the same. If your plan covers “lisinopril 10mg” but not “lisinopril-hydrochlorothiazide,” and your doctor prescribes the combo pill, you might get hit with a higher cost. Some plans only cover one version of a generic drug in a class - even if others are equally effective. That’s called “therapeutic interchange.” Third, your pharmacy might substitute a different generic without telling you. If that generic isn’t on your plan’s formulary, you could pay full price. Always ask: “Is this the exact generic my plan covers?”How to Save More on Generics

You don’t have to just accept what your plan gives you. Here’s how to take control:- Use the Medicare Plan Finder. Enter your exact medications - including generic names - and compare plans side by side. KFF found people who use this tool save an average of $427 a year.

- Look for $0 deductible plans. If you take three or more generics, skipping the deductible can save you hundreds.

- Ask for a coverage determination. If your generic isn’t covered, you can formally ask your plan to cover it. In 2023, 83% of these requests were approved.

- Check for $0 copays. Many plans now offer $0 copays for Tier 1 generics. That’s not a promotion - it’s standard.

What’s Changing After 2025

The changes aren’t over. Starting in 2026, Part D plans must include a “generic price comparison tool” in their member portals. That means you’ll be able to see, right on your phone, which generic version of your drug costs the least - even if it’s not the one your doctor prescribed. In 2029, the government will start negotiating prices for some generics. Insulin glargine (a long-acting diabetes drug) is already on the list. That could bring the cost of some generics down even further. There’s also talk in Congress about forcing plans to cover every generic in a class if they cover any one of them. Right now, a plan might cover one brand of metformin but not another. That’s confusing and unfair. If that rule passes, it’ll make things much simpler.Real Stories From People on Part D

One woman in Ohio, 72, takes five generics: for blood pressure, cholesterol, diabetes, thyroid, and arthritis. Before 2025, her monthly drug bill was $280. After hitting the $2,000 out-of-pocket cap in October, she paid $0 for the rest of the year. She didn’t know it was possible until she read her plan’s letter. A man in Florida, 68, switched plans in 2024 because his old one didn’t cover his generic heart medication. His new plan put it in Tier 1 with a $0 copay. He now saves $320 a month. He says, “I didn’t realize I was overpaying for years.” But not everyone is happy. One Reddit user reported being charged $120 for a generic blood pressure pill because his plan only covered a different generic in the same class. He had to file a coverage request - and waited six weeks for approval.What to Do Right Now

If you’re on Medicare Part D and take generics:- Log into your plan’s website or call customer service. Ask: “What tier is my generic medication on?”

- Check if your plan has a $0 deductible. If not, consider switching during Open Enrollment (October 15-December 7).

- Use the Medicare Plan Finder. Type in your exact drug names. Compare costs across plans.

- Keep your 2025 Annual Notice of Change. Mark the date when your plan changes its formulary.

- If you’re paying more than $2,000 a year for drugs, you’re likely missing the cap. Talk to your plan or call Medicare at 1-800-MEDICARE.

Are all generic drugs covered under Medicare Part D?

Almost all FDA-approved generic drugs are covered, but not every plan covers every version. Plans must cover at least two generics per drug class and at least 85% of drugs in each therapeutic category. However, they can exclude certain generics if they’re not on the FDA’s approved list or if they’re for non-covered uses like weight loss or cosmetics. Always check your plan’s formulary before switching drugs.

Why is my generic drug not covered even though it’s the same as the brand?

Plans often cover only one or two generic versions of a drug, even if others are chemically identical. This is called therapeutic interchange. For example, if your plan covers “amlodipine besylate” but not “amlodipine maleate,” you might be charged full price for the latter. You can request a coverage determination - and in 83% of cases, the plan will approve it if the drug is medically necessary.

Do I pay more for generics during the coverage gap?

No. The coverage gap - or “donut hole” - was eliminated for all drugs as of January 1, 2025. Once your out-of-pocket spending reaches $2,000, you enter catastrophic coverage and pay $0 for all covered drugs, including generics. There is no longer a phase where you pay full price.

Can I switch plans if my generic drug gets moved to a higher tier?

Yes. Each year during Open Enrollment (October 15 to December 7), you can switch to a different Part D plan that covers your medications at a lower cost. You don’t have to wait for a problem to happen. Use the Medicare Plan Finder to compare formularies and costs ahead of time.

Do I have to pay the deductible every year for my generics?

Yes, unless your plan has a $0 deductible. In 2025, the standard deductible is $615, but 52% of Part D plans offer $0 deductibles - especially those with lower monthly premiums. If you take multiple generics, a $0 deductible plan can save you hundreds. Always compare plans during Open Enrollment.

14 Comments

Billy Schimmel

December 7, 2025 AT 19:40

So basically, if you’re on lisinopril and metformin, you’re now paying less than your coffee budget? Wild.

Used to be I’d skip doses just to make the month last. Now? I just take ‘em like candy.

Ibrahim Yakubu

December 8, 2025 AT 03:08

You think this is revolutionary? In Nigeria, we pay out of pocket for EVERYTHING. No caps. No government help. If your meds cost $200/month, you either sell your goat or die. This $2,000 cap? It’s not policy-it’s a luxury. You Americans don’t even know how lucky you are.

Shayne Smith

December 8, 2025 AT 15:45

I just checked my plan-my generic statin is $0. Like, zero. I almost cried. My grandma used to cut pills in half to make them last. I’m so glad that’s over.

Andrew Frazier

December 10, 2025 AT 10:10

Oh great, now the government’s gonna pay for my pills while the illegals get free insulin. This is socialism with a smiley face. Next they’ll be handing out free Tesla’s with your prescription.

And don’t get me started on how they’re forcing plans to cover every generic. Who even decided this? Some woke bureaucrat in D.C. with no clue how markets work?

Karen Mitchell

December 10, 2025 AT 11:26

It is, of course, entirely inappropriate that the federal government should subsidize pharmaceutical expenditures for the elderly. This constitutes a moral hazard of the highest order. One must wonder: if people are no longer incentivized to economize on their medications, will adherence truly improve-or merely become a passive entitlement?

Geraldine Trainer-Cooper

December 11, 2025 AT 04:47

the cap is nice but did you know some plans still charge for the same generic if it’s in a combo pill? like if you take lisinopril + hctz instead of just lisinopril they treat it like a brand name

and no one tells you until you’re at the counter

and then you’re like wait what

and you just pay it because you’re tired

Nava Jothy

December 11, 2025 AT 13:04

Oh my GOD this is the most beautiful thing I’ve seen in my entire life 💔😭 I’ve been paying $180/month for my diabetes meds since 2018… I just cried in the pharmacy aisle… this is what justice looks like 🙏❤️

Thank you, America, for finally seeing us…

olive ashley

December 11, 2025 AT 19:39

Let me guess-this is all part of the Great Pharma Collapse. You think they’re giving you a break? Nah. They’re just waiting for you to get hooked on $0 meds so they can jack up the price of the next 50 drugs. This cap? It’s a trap. The real cost is coming in your premiums next year. Just wait.

And don’t get me started on how they’re slowly replacing generics with biosimilars that cost the same as brands. It’s all smoke and mirrors.

Mansi Bansal

December 13, 2025 AT 05:47

While I acknowledge the structural improvements in Medicare Part D formularies, I must express profound concern regarding the commodification of healthcare outcomes. The reduction of human dignity to cost-per-pill metrics is a philosophical abomination. One must ask: if a patient's life is measured in tiers and copays, has medicine ceased to be a covenant-and become merely a transaction?

pallavi khushwani

December 13, 2025 AT 11:40

i just realized… if you take 3 generics and your plan has a $0 deductible… you might hit the $2k cap in like 3 months?

so like… you’re basically getting free meds for 9 months?

that’s insane. i’m gonna check my plan right now

Dan Cole

December 14, 2025 AT 19:15

Let’s be clear: the $2,000 cap was not a gift from benevolent legislators-it was the result of relentless advocacy, data-driven lobbying, and the sheer exhaustion of seniors who could no longer afford to breathe. Anyone who dismisses this as ‘socialism’ has never had to choose between insulin and groceries. This isn’t welfare. It’s survival. And it’s long overdue.

Katie O'Connell

December 16, 2025 AT 07:44

It is curious how the formulary structure has been engineered to favor those who consume the most pharmaceuticals. One cannot help but observe that the policy incentivizes polypharmacy. Is this truly the desired outcome? Are we encouraging medical dependency under the guise of cost containment? The ethics are… questionable.

Clare Fox

December 18, 2025 AT 02:32

my mom just called me crying because her plan changed the generic they cover for her blood pressure med and now she’s paying $110 a month

she didn’t even know she could file a coverage request

and she’s 76 and doesn’t use the internet

why is this so hard

Akash Takyar

December 18, 2025 AT 07:18

Dear fellow citizens: I commend the thoughtful design of the 2025 Medicare Part D reforms. However, I urge you to remain vigilant. Always verify your formulary tier, consult your pharmacist, and document every interaction with your plan. Your health is your responsibility-and your advocacy is your power. Stay informed. Stay persistent. You are not alone.

Write a comment