Almost two-thirds of Americans take at least one prescription drug every year. If you’re one of them, your insurance plan’s coverage for medications isn’t just a nice-to-have-it’s a make-or-break factor in your health and wallet. Yet, most people don’t ask the right questions when choosing a plan. They assume their meds are covered, only to get hit with a $500 copay at the pharmacy counter. Or they don’t realize their insulin is capped at $35 under Medicare, but their other meds aren’t. Don’t be that person.

Is my specific medication on the formulary?

Every insurance plan has a list of drugs it covers-this is called a formulary. It’s not the same across plans. A drug covered by one insurer might be completely excluded from another, even within the same metal tier. Your plan might cover a generic version of your medication, but not the brand-name version you’ve been using for years. Or worse, it might cover it but only after you’ve tried three cheaper alternatives first (that’s called step therapy).Don’t guess. Go to your insurer’s website and search for your exact medication by its generic and brand names. Look for the tier it’s on. Tier 1 usually means generics and costs $10-$15. Tier 2 is preferred brand-name drugs-around $40. Tier 3 is non-preferred brands-often $100 or more. Tier 4? That’s specialty drugs like those for MS, rheumatoid arthritis, or cancer. Those can cost $1,000+ per prescription, and you might pay 25-33% coinsurance. If your drug isn’t listed at all, it’s not covered. Period.

What’s my deductible for prescriptions?

Some plans have a separate deductible just for prescriptions. Others combine it with your medical deductible. Bronze Marketplace plans, for example, often have a $6,000 deductible for everything-including your monthly blood pressure pill. That means you pay full price until you hit that $6,000 mark. A Gold plan? It might have a $150 prescription deductible. That’s a massive difference.If you take multiple medications every month, a high deductible can wipe out your savings before you even get to the copay stage. Ask: “Do I have to pay the full cost of my drugs until I meet my deductible, or is there a separate prescription deductible?” If you’re on a Bronze plan and take 3-4 prescriptions monthly, you’re probably better off switching to a Silver or Gold plan-even if the monthly premium is higher. The math often works out in your favor.

What’s my out-of-pocket maximum for drugs?

This is the most you’ll pay in a year for covered prescriptions. Once you hit it, your plan pays 100%. But here’s the catch: some plans cap your out-of-pocket costs for drugs separately from your medical costs. Others combine them. And not all plans have the same cap.For example, a Bronze plan might have a $9,450 out-of-pocket maximum for everything. A Platinum plan? Only $3,050. If you’re on a specialty drug that costs $5,000 a month, that $9,450 cap could take you just two months to hit. But if you’re on a Bronze plan with no drug-specific cap, you’re stuck paying $5,000 until you hit the $9,450 total. That’s $2,500 more than you’d pay on a Platinum plan.

Ask: “Is there a separate out-of-pocket maximum for prescriptions, and what is it?” If you’re on a high-cost medication, this number can save you thousands.

Do I need prior authorization for my meds?

Prior authorization means your doctor has to jump through hoops before the plan will pay for your drug. Maybe they need to prove you’ve tried cheaper options. Maybe they need to submit lab results. Maybe they need to explain why you can’t switch to a generic.It’s common. In fact, 28% of Medicare Part D prescriptions require prior authorization. If your plan requires it for your medication, you might get a 2-3 week delay. That’s dangerous if you’re on a drug for diabetes, heart failure, or depression. Ask: “Does my plan require prior authorization for any of my prescriptions? And how long does it usually take to get approved?” If the answer is “yes” and “it takes weeks,” consider a different plan.

What pharmacies can I use?

Your plan might cover your drug-but only if you fill it at a specific pharmacy. Many plans have narrow networks. You might think CVS, Walgreens, and your local pharmacy are all covered. But your plan might only reimburse CVS and a single regional chain. Fill your prescription at a non-network pharmacy? You’ll pay 37% more.Check the plan’s pharmacy directory. Search for your preferred pharmacy by name and ZIP code. If it’s not listed, don’t assume it’s covered. Call the insurer and ask: “Is [Pharmacy Name] in-network for my plan?” And ask if they have mail-order options. Some plans offer 90-day supplies through mail-order for a lower cost. That can save you money on maintenance drugs.

Are there coverage limits or quantity restrictions?

Some plans limit how much of a drug you can get per month. For example, they might allow only 30 pills of your painkiller per month-even if your doctor prescribes 60. Or they might require you to wait 30 days before refilling a 30-day supply.These limits are often hidden in the fine print. They’re especially common for controlled substances, mental health meds, and specialty drugs. Ask: “Is there a monthly or annual limit on the quantity of my prescriptions?” If your plan only covers 30 pills but you need 60, you’ll pay double out of pocket.

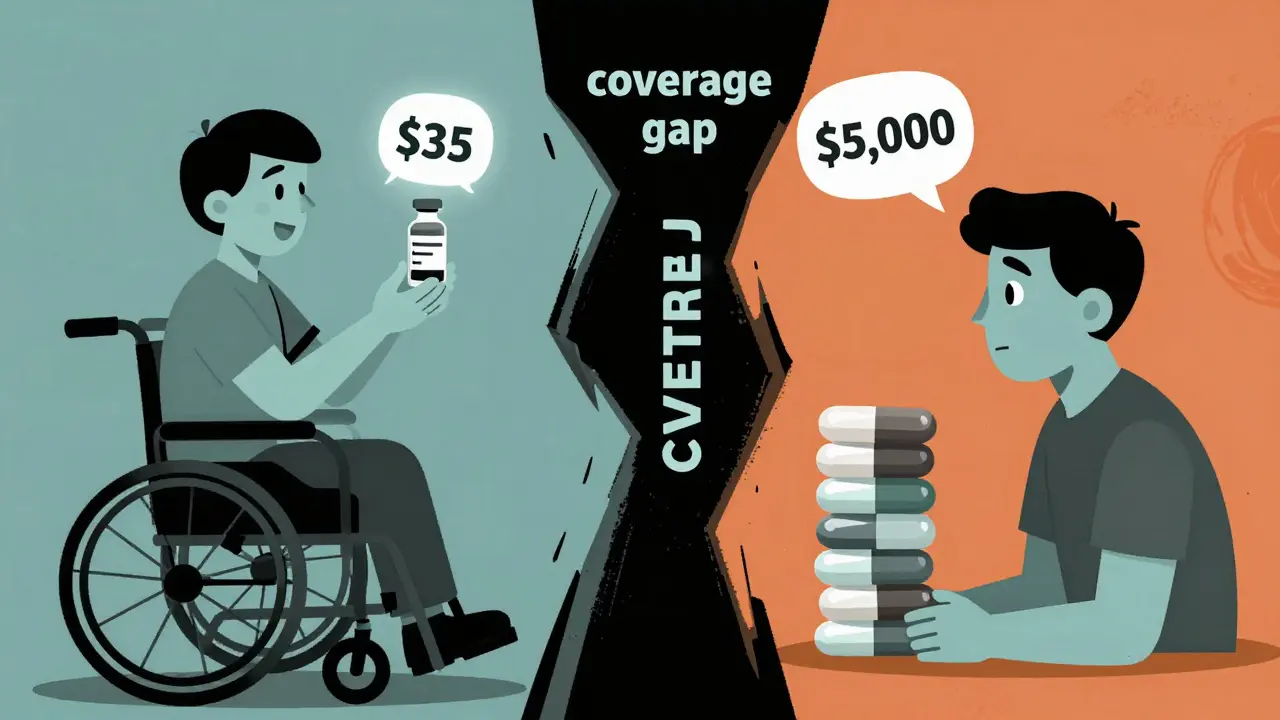

What’s the cost of my drug in the Medicare Part D coverage gap?

If you’re on Medicare Part D, you’ve probably heard of the “donut hole.” In 2024, once your total drug costs hit $5,030, you enter the coverage gap. You pay 25% of the cost until you hit $8,000. Then you get catastrophic coverage.But here’s the thing: the 25% you pay isn’t based on what you pay-it’s based on the drug’s list price. That means if your drug costs $1,200 and you pay $300, that $300 counts toward getting you out of the gap. But if your drug is $1,200 and you only pay $150 because of a coupon, only $150 counts. That’s a trap.

Ask: “How does the coverage gap work for my specific drugs?” And don’t rely on the plan’s online calculator. Call customer service and give them your exact medications. They’ll tell you where you’ll hit the gap and what you’ll pay.

What’s changing in 2025?

Big changes are coming. Starting in 2025, Medicare Part D will have a $2,000 annual out-of-pocket cap for all drugs. Insulin will cost no more than $35 per month. And the coverage gap will disappear. That’s huge.But if you’re on a Marketplace plan, nothing changes for you yet. The Inflation Reduction Act doesn’t apply to private insurance. So if you’re under 65 and on a private plan, your out-of-pocket costs could still hit $10,000 a year. That’s why it’s even more important to compare plans now. If you’re on a high-cost drug, a Gold or Platinum plan might be worth the extra $200-$400 monthly premium. You could save $1,800+ a year.

When should I check this?

If you’re on a Marketplace plan, check your coverage during Open Enrollment: November 1 to January 15. Use the HealthCare.gov plan comparison tool. Enter your medications and preferred pharmacy. It’ll show you total annual costs, including premiums, deductibles, and copays.If you’re on Medicare, use the Medicare Plan Finder during the Annual Election Period: October 15 to December 7. Enter your drugs by their NDC codes (you can find them on the bottle). Don’t just pick the cheapest premium. Pick the plan with the lowest total cost for your meds.

And if you’re switching plans mid-year because your drug was dropped or your pharmacy changed? You have a special enrollment period. Don’t wait until you’re out of pills. Act fast.

What to do if your drug isn’t covered

If your medication isn’t on the formulary, you have options. First, ask your doctor if there’s a similar drug on the formulary. Sometimes switching to a different brand or generic can save you hundreds.If not, you can file an exception request. Submit a letter from your doctor explaining why you need this specific drug. You might get approved. If you don’t, you can appeal. The process can take weeks, but it’s worth it for life-saving meds.

And don’t forget about patient assistance programs. Many drug manufacturers offer free or low-cost meds to people who qualify. Check NeedyMeds.org or the manufacturer’s website.

Don’t skip this step. Skipping your meds because of cost doesn’t save money-it costs more in the long run. Hospital visits, ER trips, and complications from untreated conditions add up fast.

What if my prescription isn’t on the formulary at all?

You can request an exception from your insurer. Your doctor must write a letter explaining why you need this specific drug-usually because alternatives didn’t work, caused side effects, or aren’t medically appropriate. If approved, the plan will cover it. If denied, you can appeal. Don’t assume it’s impossible-many exceptions are granted.

Can I use a coupon or discount card with my insurance?

It depends. For Medicare Part D, manufacturer coupons don’t count toward your out-of-pocket costs in the coverage gap. For private insurance, some plans allow them, others don’t. Always ask your pharmacist: “Will this coupon reduce what I pay now, or just lower the list price without helping my deductible?”

Why does my drug cost more this year even though I’m on the same plan?

Formularies change every year. Your drug might have moved from Tier 2 to Tier 3. Your deductible might have increased. Or your insurer might have switched to a different pharmacy network. Always check your plan’s annual notice of changes-it’s mailed to you every fall.

Is it better to get prescriptions through mail order or in-store?

Mail order is often cheaper for maintenance drugs like blood pressure or diabetes meds. Many plans offer 90-day supplies with a lower copay than 30-day fills at a local pharmacy. But if you need your med right away, or your doctor adjusts your dose often, in-store might be better. Check your plan’s rules-some require mail order for specialty drugs.

Do all insurance plans cover the same drugs?

No. Even two Gold plans from different insurers can have completely different formularies. One might cover your antidepressant with a $10 copay. Another might not cover it at all. Always compare formularies side by side before choosing a plan.

Final tip: Don’t wait until you’re out of pills

The average person spends 20 minutes checking their prescription coverage during open enrollment. Those people save $1,147 a year on average. The people who skip it? They pay more, stress more, and sometimes go without meds.Take 20 minutes. List your drugs. Check your pharmacies. Compare plans. It’s not glamorous. But it’s the difference between paying $3,000 a year for insulin-or $35.

9 Comments

Peyton Feuer

January 4, 2026 AT 06:23

just found out my insulin is $35 but my anxiety med is $400 a month… how is this even legal?

Siobhan Goggin

January 5, 2026 AT 05:19

This is the most practical guide I’ve read all year. I wish my doctor had given me this checklist instead of just handing me a script and saying ‘take it.’

Jay Tejada

January 6, 2026 AT 07:55

lol so you’re telling me the system is designed to make you choose between food and meds? genius. absolute genius.

Allen Ye

January 7, 2026 AT 16:52

What this post reveals isn’t just a flaw in insurance-it’s a failure of the social contract. We’ve normalized the idea that health is a commodity to be bargained for, not a right to be guaranteed. The formulary isn’t a clinical tool-it’s a gatekeeping mechanism disguised as cost control. When your life depends on a pill and the only thing standing between you and it is a tier system, you’re not in a healthcare system-you’re in a marketplace where your body is the product. And the people who designed this don’t have to pay the copay. They get to write the rules from their corner offices while someone’s child skips doses because the $1,200 drug got moved from tier 2 to tier 4. This isn’t inefficiency. This is intentional cruelty wrapped in bureaucracy.

John Wilmerding

January 8, 2026 AT 12:44

Thank you for this comprehensive breakdown. I’d like to emphasize one additional point: many patients are unaware that they can request a formulary exception even if their medication is not listed. The process requires a letter of medical necessity from the prescribing provider, but it is often successful-especially when supported by clinical evidence or prior treatment history. Additionally, some plans offer temporary coverage while the exception is under review. Always ask your pharmacy to initiate the process; they are trained to assist with this. Do not accept a flat ‘no’ without escalating it formally.

Also, be sure to review the Annual Notice of Changes (ANOC) mailed to you each fall. Insurers are required to notify you of formulary, tier, or cost changes. Many people overlook this document, assuming their coverage stays the same. It does not. A drug that was $20 last year could become $200 this year without warning if you don’t check.

Finally, if you’re on Medicare, use the official Medicare Plan Finder tool-not third-party sites. It pulls live data from CMS and includes all cost-sharing details, including the coverage gap. Even small differences in pharmacy networks can add up to hundreds in annual savings.

Brendan F. Cochran

January 9, 2026 AT 07:14

you people complain about drug prices but you don’t know how to spell ‘formulary’ and you think the government should fix it for you. get a job, pay taxes, stop being lazy. if you can’t afford your meds, maybe you shouldn’t be on them. my cousin’s brother took a $500 pill and died of an overdose-probably because he was on welfare. don’t be that guy.

Jason Stafford

January 9, 2026 AT 12:21

EVERY SINGLE ONE OF THESE QUESTIONS IS A TRAP. THE INSURANCE COMPANIES KNOW YOU’LL NEVER ASK THEM. THEY WANT YOU TO THINK YOU’RE IN CONTROL WHEN YOU’RE JUST A NUMBER IN THEIR ALGORITHM. THEY CHANGE FORMULARIES AT MIDNIGHT. THEY REMOVE DRUGS WITHOUT NOTICE. THEY MAKE YOU CALL 12 TIMES JUST TO GET A SIMPLE ANSWER. AND THEN THEY SEND YOU A FORM THAT’S 17 PAGES LONG WITH FINE PRINT THAT SAYS ‘WE RESERVE THE RIGHT TO DENY WITHOUT REASON.’ THIS ISN’T HEALTHCARE. THIS IS A SCAM RUN BY WALL STREET WITH A WHITE COAT ON.

I’VE BEEN ON 4 DIFFERENT PLANS IN 3 YEARS. EVERY TIME I THINK I’VE FIGURED IT OUT, THEY CHANGE THE RULES. I’M NOT EVEN TALKING ABOUT THE PHARMACIES THAT ‘APPROVE’ YOUR RX AND THEN TELL YOU AT THE COUNTER ‘OH WE DON’T HAVE IT’ AND MAKE YOU WAIT 3 DAYS. THIS SYSTEM IS BROKEN. AND NO, ‘CHECKING DURING OPEN ENROLLMENT’ WON’T FIX IT. THEY’RE ALWAYS CHANGING THE GOALPOSTS.

josh plum

January 10, 2026 AT 14:14

you know what’s worse than high drug prices? People who think they deserve free medicine. If you can’t afford your prescriptions, maybe you shouldn’t have had kids. Or gotten sick. Or lived past 40. I work 60 hours a week and I pay for my own meds. You think the system’s unfair? Maybe you should’ve planned better. This isn’t a right-it’s a privilege you earn by being responsible.

mark etang

January 12, 2026 AT 06:16

Thank you for this essential guidance. It is imperative that all policyholders conduct a thorough review of their prescription coverage during the annual enrollment period. The financial implications of overlooking even minor formulary changes can be catastrophic. I strongly encourage all individuals to consult with a certified health benefits advisor and utilize the official plan comparison tools provided by federal and state exchanges. Proactive engagement with one’s healthcare plan is not merely prudent-it is a moral obligation to one’s own well-being and to the broader healthcare ecosystem.

Write a comment